Gold is hovering around $4,500 per ounce. Central banks have purchased more than 1,000 tonnes annually since 2022. This is not a hedge trade or a policy reaction. This is a structural reallocation of global reserves, and it shows no sign of slowing down.

The effect on the gold price has been historic.

But the more important story, the one most investors haven’t fully grasped just yet, is what that gold price has done for the companies that produce it.

In 2025, the world’s six largest gold producers – Newmont,1 Agnico Eagle,2 Barrick,3 AngloGold Ashanti,4 Gold Fields5 and Kinross6 – brought in just under $24 billion in free cash flow.

Read that again. Six companies. One year. Nearly $24 billion in free cash flow in a single year.

The problem for producers is existential: reserves deplete and quality replacement assets are scarce. The solution is acquisition.

In January 2026, Fresnillo, the world’s largest primary silver producer, paid C$780 million to acquire Probe Gold at a 39% premium to market.7

That was not a one-off. It was the opening move in a revaluation of the entire developer tier. Sophisticated buyers are not waiting for the mainstream to figure this out.

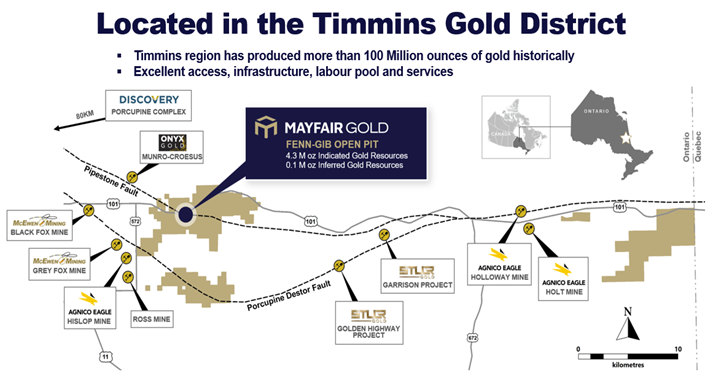

Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) has 4.3 million ounces in Ontario’s Timmins Gold District,8 a region that has produced over 100 million ounces of gold and counts Agnico Eagle, Kinross, and Pan American Silver among its neighbors.

Ontario is the #1 mining jurisdiction in Canada and #2 globally, per the Fraser Institute.

And in April 2026, the company expanded its land package by more than 65% with the acquisition of three properties from Plato Gold, all along the Porcupine-Destor Fault Zone, the most prolific gold-controlling structure in the district.9

The Pre-Feasibility Study is complete.10 The permitting path is clear. The team has built billion-dollar companies twice. The market has not caught up yet. That gap is the opportunity.

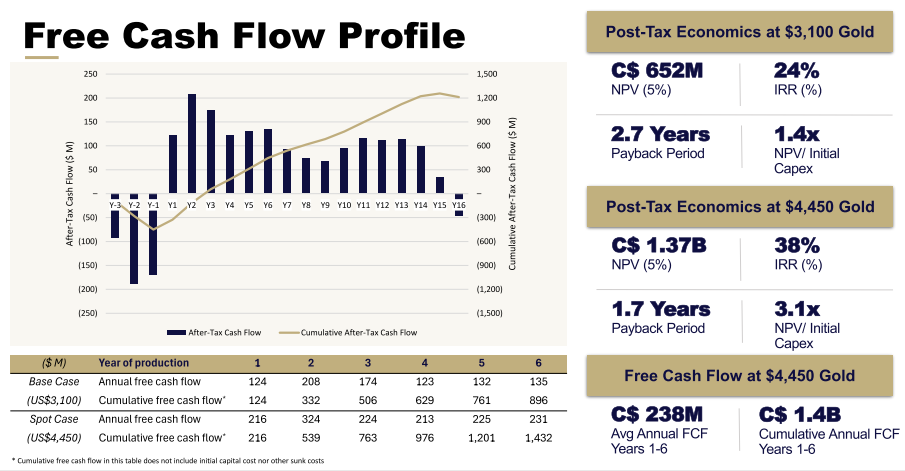

A C$652M NPV at US$3,100 Gold. Gold Is Now $4,500.

In January 2026, Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) released the NI 43-101 Pre-Feasibility Study.11 The numbers were conservative when published. At current gold prices, they are substantially more compelling.

At the PFS base case of US$3,100/oz: after-tax NPV of C$652 million, IRR of 24%, payback in 2.7 years on C$450 million of initial capital.

At the January 2026 spot price of US$4,450/oz: NPV rises to C$1.37 billion, IRR climbs to 38%, payback falls to 1.7 years.

Every US$100 move in the gold price adds approximately C$50 million to the NPV. Gold has moved more than US$1,400 above the PFS base case since those numbers were set. The economics published in January 2026 are a floor, not a ceiling.

Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) mine plan is built on only 1.04 million ounces of Probable Reserves, just 24% of the 4.3 million ounce Indicated Resource.

The remaining 3.3 million ounces are not in the current plan. They carry no assigned value in the PFS. They represent pure reinvestment optionality that grows more valuable with every step the company takes to get closer to cash flow.

Base Case US$3,100/oz Gold (C$1.35:US$1 Exchange Rate)

After-Tax NPV (5%): C$652 million | After-Tax IRR: 24% | Payback: 2.7 years

Initial Capex: C$450 million | Sustaining Capex: C$61 million

Avg Annual Production, Years 1 to 6: 71,336 oz Au at 1.47 g/t feed grade

AISC, Years 1 to 6: US$1,171/oz | LOM AISC: US$1,292/oz

Cumulative FCF, Years 1 to 6: C$896 million | Cumulative LOM FCF: C$1.7 billion

Spot Gold Scenario US$4,450/oz (as of January 6, 2026)

After-Tax NPV (5%): C$1.37 billion | After-Tax IRR: 38% | Payback: 1.7 years

Avg Annual FCF, Years 1 to 6: C$239 million | Cumulative FCF, Years 1 to 6: C$1.43 billion

Grade control drilling results are making the early-year numbers look even better. Preliminary data from 56 tight-spaced holes in the Phase 1 starter pit showed actual grades of 2.21 g/t gold versus the 1.68 g/t block model prediction at a 0.8 g/t cut-off. The highest-margin years of the mine may carry grades materially above current plan assumptions.

Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) expects final assays in April 2026, and a positive reconciliation result would be a meaningful near-term catalyst.

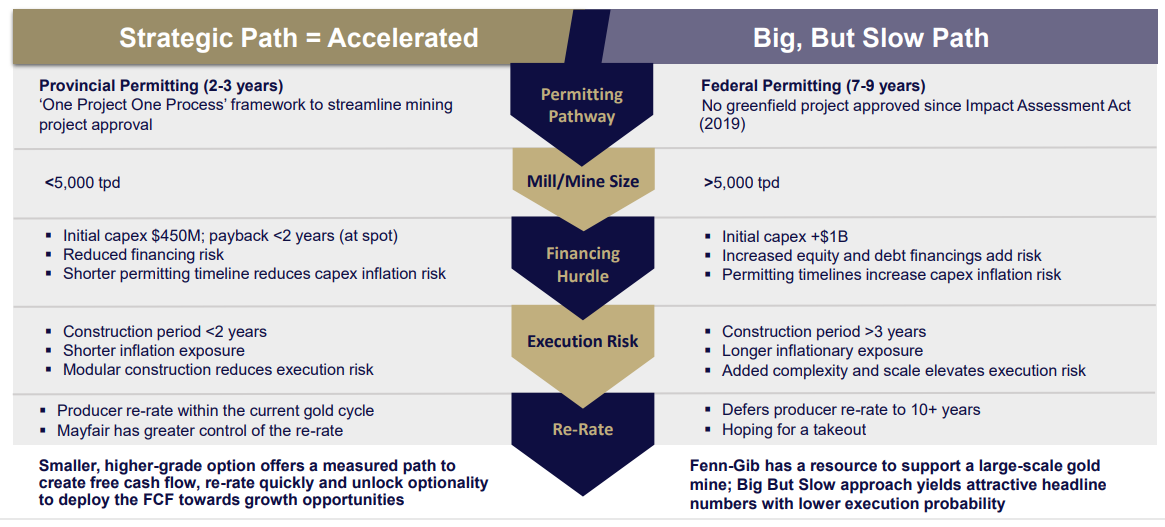

The Permitting Edge No Developer in This District Can Match

The Fenn-Gib mine plan was deliberately designed below 5,000 tonnes per day. That was the single most important strategic decision Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) has made, and it is one no competitor who designed for a larger throughput can replicate.

Projects below 5,000 tpd qualify for Ontario’s provincial permitting process under the One Project, One Process framework: a permitting pathway designed to get mines approved within 24 months. The federal Impact Assessment Act, the only alternative, has not approved a single greenfield mine in Canada since 2019. That process takes 7 to 9 years and carries no guarantee of outcome.13

Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) filed its Notice of Project Status on February 5, 2026.14 Admission into the 1P1P framework is targeted for summer 2026. Construction is targeted for 2028. Initial production is targeted for 2030.

Companies that have navigated this pathway successfully have seen it serve as a meaningful re-rating event in its own right. Most developers in this district are staring at a decade of federal permitting uncertainty. Mayfair is targeting under two years. That is not a minor detail. That is the entire re-rating thesis.

The Team That Has Actually Done This

Drew Anwyll is not offering a promotional statement. He is making a professional commitment backed by a career that includes building Detour Lake, the largest open pit gold mine ever constructed in Canada, from a greenfield site. He also led the Marathon PGM Project through a joint federal-provincial environmental assessment in Ontario. Nobody has more direct experience building this specific type of mine in this specific jurisdiction.

Strategic Advisor Pierre Beaudoin served as COO of both Detour Gold and SilverCrest Metals and delivered the Las Chispas mine ahead of schedule and below budget. The team around this asset has done every part of this job before, in harder markets, with less certainty than exists today.

Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) listed on the NYSE American exchange on January 27, 2026 under the ticker MINE, opening the company’s story to a substantially broader base of US institutional investors who are discovering it for the first time.15

The Shareholder Base Is the Signal

Most junior mining companies survive on retail capital. Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) attracted a very different kind of investor.

Muddy Waters Capital and Carson Block: 16% Combined Ownership.16 Carson Block built Muddy Waters into one of the most feared names in global finance. Bloomberg Markets has called him one of the most influential figures in global finance.17 His entire professional reputation is built on finding what is wrong with a company.

Based on reported holdings, Muddy Waters Capital and Carson Block hold over 16% of Mayfair’s share register, pointing to a significant level of alignment with the Fenn-Gib story.

Oaktree Capital Management: C$14.85 million invested. In September 2025, Howard Marks’ $200 billion generalist institution acquired 9 million shares (4.5M after share consolidation) of Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) in a single transaction.18 Oaktree is not a gold fund or a resource specialist. Generalist institutions of this caliber invest when a business development strategy is compelling enough to stand on its own merits. Nearly C$15 million from Oaktree is an endorsement that virtually no company of this size can claim.

Heeney Capital: co-founders who have never left. Sean Pi and Henry Heeney, both Partners at Heeney Capital, co-founded Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) in 2019 and both sit on the board today.19 They built this company and have held their position through the proxy battle, the management turnaround, and every challenge in between. That continuity of conviction is its own form of due diligence.

Vestcor: the institutional investment manager for several Canadian pension funds and Nokomis, a Dallas-based long/short equity hedge fund, round out a shareholder base where mining specialists, pension capital, generalist institutions, and the world’s most forensic short seller all arrived at the same conclusion independently.20

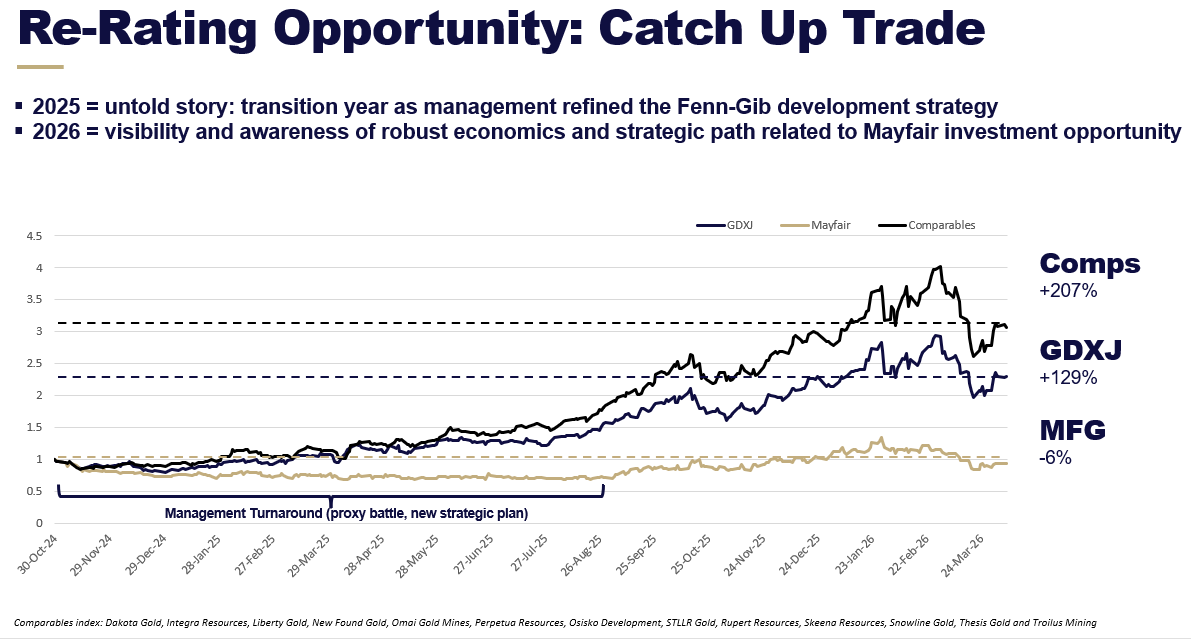

The History of What Happens Next

An analysis of 14 single-asset gold developers that successfully brought mines into production shows average price appreciation of 176% from permitting through 18 to 24 months post-production, approximately 146% outperformance versus the GDXJ gold miners index.21

The names most directly comparable to Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) are not hypothetical.

Artemis Gold, delivered +427% versus the GDXJ after reaching production in May 2025. Atlantic Gold returned +424%. Victoria Gold returned +521%.

Each was a focused developer with a real asset in a Tier-1 jurisdiction and a team that had executed before. Each re-rated dramatically once the market recognized the transition to producer was real.

Mayfair Gold is flat% since October 2024. The GDXJ is up 129% over the same period. Its comparable developer peer basket is up 207%. The gap is not a reflection of the asset quality. It is a reflection of a story the broader market has not fully discovered yet.

The Setup in Plain Terms

✓ 4.3 Moz Indicated Resource: 181.3 Mt at 0.74 g/t Au, 97% confidence, 300,000+ metres drilled (NI 43-101, effective September 3, 2024)

✓ Completed 2026 Pre-Feasibility Study: C$652M NPV (5%), 24% IRR, 2.7-year payback at US$3,100/oz gold

✓ Spot gold scenario: C$1.37B NPV (5%), 38% IRR, 1.7-year payback at US$4,450/oz

✓ 1.04 Moz Probable Reserve @ 1.29 g/t Au: only 24% of the total resource in the current mine plan

✓ Grade control drilling: 2.21 g/t actual vs. 1.68 g/t block model at 0.8 g/t Au cut-off (preliminary)

✓ Ontario provincial permitting pathway, 18 – 24 months vs. 7 to 9 years federally

✓ Notice of Project Status filed February 5, 2026, 1P1P admission targeted summer 2026

✓ Construction target 2028, initial production targeted 2030

✓ C$450M initial capex with C$35M cash on hand: fully funded through most of the permitting phase

✓ AISC of US$1,171/oz in Years 1 to 6, among the most competitive open pit cost structures in Canada

✓ Highway 101 site access power grid within 10 km, Timmins regional workforce

✓ Exploration Upside. Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) recently expanded its land holdings by more than 65% with the acquisition of three properties from Plato Gold, all along the Porcupine-Destor Fault Zone. Exploration is a concurrent strategy to mine derisking, with the goal of growing the resource and improving mill feedstock grade. More exploration news is expected soon.

✓ 34% insider ownership, C$19M in management and insider stock purchases since October 2024

✓ Oaktree Capital Management (C$14.85M), Muddy Waters, Heeney Capital, Vestcor, Nokomis as anchor shareholders

✓ NYSE American listing (MINE) expanded US investor access as of January 27, 2026

✓ Management track record: SilverCrest $15M → $1.5B; Artemis Gold $5/share → $40/share

✓ Currently trading at ~$50 EV/oz vs. producers at $1,000to$2,000 EV/oz

The Window Is Open. Windows in Gold Don’t Stay Open Long.

The grade control assays are incoming. The 1P1P admission decision is targeted for this summer.

Mayfair Gold just expanded its land package by more than 65%, adding three new properties along the Porcupine-Destor Fault Zone. Exploration is live. More news is coming.

A new NYSE listing is only beginning to bring this story to US institutional investors for the first time.

The catalyst stack is active and building in real time. The companies that get discovered before the mainstream tend to generate the most compelling outcomes for those paying attention early. Mayfair Gold Corp. (AMEX:MINE) (TSXV:MFG) is at exactly that inflection point.